Do you have an emergency fund ?

If you don’t have a medical emergency fund then you need to buy a health insurance today itself.

You can ONLY buy a good policy when you are fit and healthy. Lets try to understand important concepts of Health Insurance, incase you get confused; do ping me on 9544836262.

Waiting Periods

Most of the insurance plans will have the three waiting periods:

1. Initial; 30 Day Waiting Period

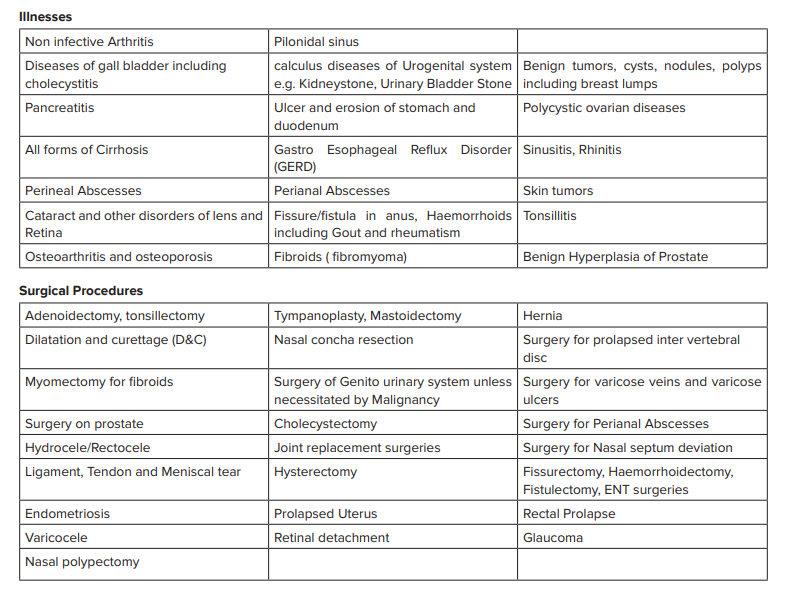

2. Two Year waiting for slow growing illness like cataract, Ulcer etc; See the below snapshot

3. Three year waiting period for all the illness that we have before buying the policy, if you are diagnosed with critical illness related to brain or heart, getting a good plan will be difficult. Waiting for certain lifestyle diseases like Diabetes, High Blood Pressure, Cholesterol etc can be reduced by paying extra for riders.

Permanent Exclusion

Most of the insurers don’t cover Maternity Costs, OPD Expenses, Fertility Treatments, Weight Loss Procedures Etc. Search for Standard Exclusions in the Policy Wordings for the complete list.

Premiums

- Premiums will increase every year depending upon the plan that you chose; you can expect 4-5% increase.

If you plan has age brackets like 15 to 25, 26-30 etc, then you can expect an increase of 15-20% - Your premiums will increase if the inflation is higher; this normally happens once in 2-3 years.

- If you have any medical condition or illness while buying the policy, premiums can be increased in the range of 10-40% depending on the company you chose. These are called LOADING CHARGES.

Bonus or No Claim Bonus

A good plan will have a great bonus structure; for example 50% of base cover as bonus in second and third year even if you make a claim. The bonus shouldn’t have any conditions or linked to CLAIMS.

Most of the new age plans will give you bonus even if you claim. A good bonus structure will help you to cover medical costs for the next 5-10 years.

Lets see an example of bonus structure in a plan called Optima Secure from HDFC Ergo.